July 11: The Day a Bank Died (and What It Still Teaches Us)

Seventeen years ago today, on July 11, 2008, a bank with over $30 billion in assets collapsed almost overnight.

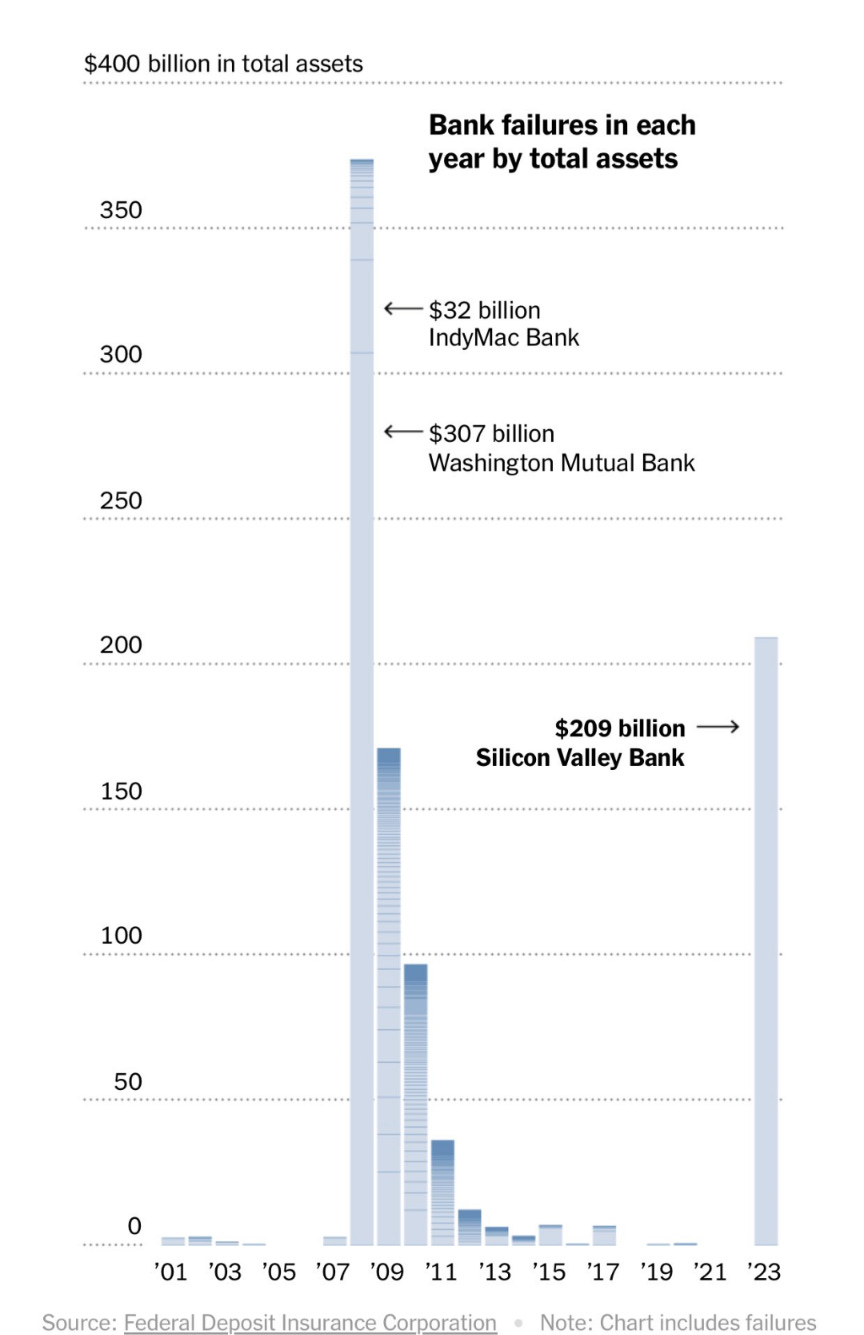

IndyMac Bank, once the 7th largest savings and loan institution in the U.S., was seized by federal regulators in what became one of the most dramatic failures of the 2008 financial crisis.

It wasn’t sudden. The warning signs had been flashing for months.

But like most financial disasters, it wasn’t the balance sheet that brought IndyMac down — it was the loss of trust. And once that trust evaporated, the collapse was inevitable.

The numbers alone were staggering:

$32 billion in assets

$19 billion in total deposits

$1.3 billion withdrawn in just 11 days before the shutdown

Over 10,000 borrowers in default or foreclosure by late 2008

And yet, most people saw it coming — and ignored it.

What Was IndyMac?

IndyMac Bancorp, based in Pasadena, California, started as a spinoff from Countrywide. It ballooned into the 7th largest savings and loan in the U.S., focused heavily on Alt-A mortgages (loans made to borrowers with better credit than subprime, but with limited documentation or income proof).

Its business model was simple:

Offer low-doc or no-doc mortgages

Sell the loans into mortgage-backed securities (MBS)

Pocket the fees, repeat

For a while, it worked.

Then the MBS market froze in late 2007.

And suddenly, IndyMac was stuck with a toxic loan book it couldn’t sell, and no more capital coming in.

The Fuse: Public Panic and a Classic Bank Run

The final blow came from a very modern spark:

On June 26, 2008, Senator Chuck Schumer publicly released a letter raising concerns about IndyMac’s solvency.

That was enough to trigger a run on the bank. In under two weeks, over $1.3 billion in deposits vanished.

By July 11, 2008, the FDIC had no choice but to step in. Lines of panicked customers formed outside branches. IndyMac was gone.

Why It Collapsed — A Breakdown

1. Poor Underwriting Standards

Heavy reliance on Alt-A loans (over 80% of loan originations by 2007)

Many loans made with no income verification (aka “liar loans”)

High loan-to-value (LTV) ratios, especially in overheated housing markets

2. Excessive Leverage

Total assets of $32 billion with thin Tier 1 capital

High dependence on short-term wholesale funding (not sticky deposits)

3. Overexposure to Real Estate

90%+ of its loan book was tied to residential mortgages

Vulnerable to any downturn in housing — and housing was crashing

4. Failed Securitization Model

IndyMac was originating to sell, not to hold

When buyers of MBS disappeared, IndyMac was stuck with billions in exposure

Here’s a snapshot of what the FDIC reported post-collapse:

Losses to the FDIC insurance fund: $10.7 billion

Over 10,000 employees laid off

50,000+ foreclosures linked to IndyMac-originated loans

Net loss for 2007 alone: $508 million

Share price in 2007: $45 → in July 2008: $0.28

The FDIC set up a bridge bank and eventually sold the remnants to a group led by Steve Mnuchin (which later became OneWest Bank).

How the System Has Changed Since 2008

After the crisis, reforms came fast and hard:

Capital & Liquidity Requirements

Basel III introduced stricter Tier 1 capital ratios and Liquidity Coverage Ratios (LCR)

U.S. banks now undergo stress tests and CCAR reviews by the Fed

Mortgage Lending Standards

Dodd-Frank banned most no-doc lending

The Qualified Mortgage (QM) rule ensures lenders verify income and ability to repay

FDIC Deposit Coverage Awareness

Insured deposit limits raised from $100,000 to $250,000

Most individuals today are far more aware of FDIC protection

But New Risks Have Emerged (2023–2025)

Digital Bank Runs

In March 2023, Silicon Valley Bank (SVB) collapsed after $42 billion in withdrawals in a single day

Mobile banking, social media, and group chats can drain a bank faster than regulators can respond

Duration Mismatch & Interest Rate Risk

SVB and others held long-dated securities bought during the low-rate era

When the Fed hiked aggressively in 2022–2023, bond prices fell, creating unrealized losses that wiped out equity when withdrawals surged

Shadow Banking Risks

Non-bank lenders now control a massive share of U.S. credit markets

These entities aren’t subject to the same regulation or capital standards, creating systemic fragility outside the traditional banking system

IndyMac’s Core Lesson Still Applies Today

Despite the reforms, the financial system still runs on confidence.

When that confidence cracks — whether from bad loans or bad headlines — no amount of regulation can stop the bleed.

IndyMac taught us that liquidity is never guaranteed. It’s a function of trust.

And trust can vanish fast.

When a bank or a system loses the trust of its customers or counterparties, it can unravel fast, no matter how solid the numbers look on paper.

IndyMac, SVB, First Republic... the names change. The mechanics don’t.

If you’re in finance or building wealth:

Know what backs your bank

Understand the asset-liability mix

Watch for concentration risk

Stay under FDIC coverage limits where possible

Don’t blindly trust yield. Ask what risk it hides

Final Thought: Don’t Just Watch Markets. Watch Risk.

Today, July 11, isn’t just a footnote in banking history.

It’s a reminder.

A reminder that collapses start slow, and end fast.

That poor risk management doesn’t hurt until it suddenly does.

And that the banking system — no matter how advanced — is only as strong as the decisions behind it.

So whether you’re managing money, running a business, or just trying to grow your wealth, stay curious. Stay cautious. Stay liquid.

The information in this post is for educational and informational purposes only. It reflects the author’s personal research and analysis, which may be subject to error or omission. This is not financial, investment, or trading advice. Always conduct your own due diligence and consult with a qualified financial advisor before making any investment or trading decisions.