Why Arm’s Temporary Pullback Is Your Entry Opportunity

High-margin licensing meets technical support at a price worth watching.

ARM 0.00%↑ ’s shares have surged since April, riding the AI & IoT wave. After a brisk 40% rally from $80 to $168, the stock is digesting gains. This pullback masks a potential long-term buying opportunity in one of the semiconductor sector’s most innovative companies.

Key Takeaways

Arm Holdings, the leading designer of semiconductor IP, boasts exceptional revenue growth, high-margin licensing royalties, and robust free-cash-flow generation.'

Its shares have pulled back from recent highs into a shallow correction that aligns with key Fibonacci support and an oversold momentum reading.

From a fundamental vantage, Arm’s secular tailwinds in AI and IoT underpin double-digit growth forecasts; technically, it’s consolidating within an overall up-trend.

A disciplined entry on confirmation of support, ideally in the $140–$145 area, offers attractive asymmetric upside toward $180–$220 over the next 12–24 months.

Fundamental Analysis

1. Business Model & Market Position

Pure-play IP licensing: Arm designs and licenses chip architectures and collects royalties on each chip shipped. This “land-and-expand” model gives high gross margins (80–95%¹) and attractive operating leverage.

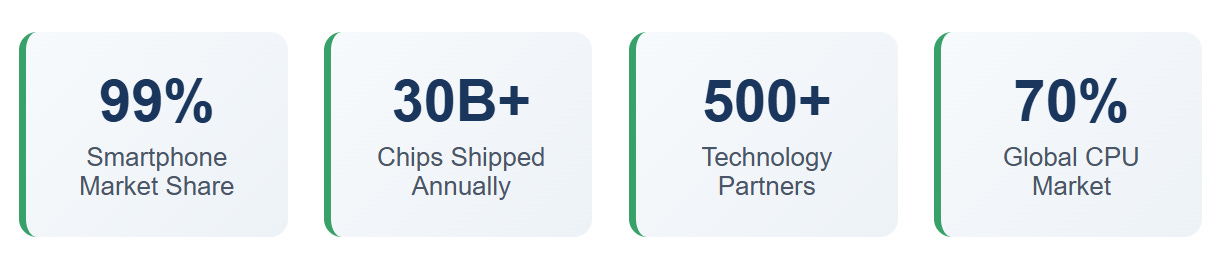

Leadership in AI & IoT: Arm’s designs power >70% of the world’s smartphones, billions of IoT devices, and are now central to edge-AI and data-center GPU/CPU deployments. Their architecture is winning share among hyperscalers and GPU innovators.

2. Recent Financial Performance

(All figures in USD billions)

Revenue Growth: 2021–24 CAGR ~35% (from ~$2.5 B to ~$5 B). License fees and royalties both expanding in double digits.

Margins & Cash Flow: Gross margin ~90%; operating margin in 30–35% range; FCF conversion >100% of net income due to light capex.

Balance Sheet: Net cash position (cash > debt), ample liquidity for R&D investment and possible bolt-on acquisitions.

3. Analysts’ Forecasts & Valuation

Consensus EPS Growth: Forecasts call for ~20–25% annual EPS growth through FY2027.

Current Multiple: Trading around 50× forward EPS; premium reflects secular growth but requires sustained execution.

Catalysts: New CPU license wins, data-center royalty ramp, improved client diversification beyond smartphones.

In a world of commoditized silicon, IP becomes king—and cash flow follows.

Technical Analysis

Timeframes: We’ll look at the daily chart for trend & levels, then the 2-hour and 1-hour for entry refinement.

1. Overall Trend & Key Levels (Daily)

Primary Uptrend: Since the April 2025 low (~$80), ARM has staged a textbook 5-wave Elliott impulse, peaking near $168.

Fibonacci Retracements:

0.236 pullback at $124.8 (already reclaimed long ago).

0.382 at $109.3 (too deep for current correction).

0.618 at $102.3 (unlikely in a healthy trend).

Recent correction from the July peak has retraced only ~12%, just beneath the 0.236 zone of the smaller June–July swing ($152→$168).

Moving Averages:

50 SMA (now $148) and 100 SMA ($154) are above price, acting as dynamic resistance turned support.

200 SMA (~$133) resides below current correction lows.

Momentum:

RSI (14) dipped into the low-40s on the daily, not yet oversold (<30), suggesting more room to run.

MACD: Histograms contracting below signal, correction in progress but no bearish divergence witnessed historically.

2. Intermediate Support & Entry (2-Hour)

Short-term Fib of July swing ($152→$168):

0.382 → $158.3

0.618 → $162.1

Current price ($146.9) has broken below that mini-swing’s 0.236 ($155.8) and is nearing the 50 SMA of the 2-hour ($148).

Trendline & SMAs:

A rising trendline from early May sits near $144–$145.

Confluence area at $140–$145: 200 SMA (2-hr), trendline support and the low end of the daily SMAs.

Short-term Oscillators:

2-hr RSI is oversold (<30) and turning up.

MACD just began a small positive triangle, hinting at a potential bounce.

Buyers often step in when sentiment is cooling but the long-term trend stays intact.

Our Investment Plan

1. Positioning & Entry

Core Entry Zone: $140–$145. Scale in ⅓ there.

Secondary Entry: If the 200 SMA (daily, ~$133) is tested and holds, add another ⅓.

Confirmation: Look for a bullish reversal candle and rising small-timeframe volume or RSI cross above 30.

2. Targets & Stops

First target: $168 (recent high) – covers ~+15%.

Secondary target: $180–$190 (1.618 fib extension of the June rally).

Long-term stretch: $210–$220 (2.618–3.618 extension zone, reflecting multi-year growth).

Initial stop: Below $138 (just under the entry range). Trailing stop to 8–10% as trade advances.

3. Risk Management

Position size no more than 3–5% of total portfolio initially.

Reassessment if ARM closes below $133 (200 SMA daily).

Plan the trade, then trade the plan, always respect your stops.”

Bottim Line

Arm Holdings sits at the crossroads of structural semiconductor growth, powered by AI, 5G, and IoT demand. Fundamentally, its high-margin licensing model and robust FCF generation support premium valuation, provided it continues to win data-center and edge compute design contracts. Technically, ARM remains in a powerful up-trend despite a healthy pullback into confluence support around $140–$145.

For medium–long-term investors, initiating on dips with disciplined stops and a multi-leg scale-in can yield attractive asymmetric upside. If price decisively breaks below the $133 level on rising volume, it would signal a deeper trend change and warrant pause. Otherwise, the secular trajectory remains your friend.

Quality growth at a reasonable correction: that’s where opportunity lies.